Introduction

I have chosen to focus on discussing topic 1 (Financialisation) and topic 6 (Critical drivers of the modern business environment), including discussing why these topics are important in contemporary business, by using the NHS as an example where I have previously worked as a Doctor. I will be dividing this essay in to two sections, first focussing on financialisation and how it is impacting the NHS, and secondly focussing on the critical drivers for modern day business and how these are being implement in the NHS.

Topic 1-Finanancialisation

In the last thirty years, and more the world economy has undergone rapid transformations. The role of the government is diminishing while that of markets has increased; domestic and internal financial transactions have grown remarkably, including economic transactions between countries have been on the rise. This changing landscape has been characterised by the rise of neoliberalism, globalisation and financialisation. (Epstein, 2005) A system of financial capitalism has emerged in which companies are viewed as merely assets to be bought and sold, and vehicles for maximising profits through financial strategies. (Batt R et al, 2013) The financial strategies for marking profits without regard to the effects organisational productivity, quality, or long term competitiveness include trading, buying and selling companies or divisions of companies, selling off assets, and using debt for tax advantages or share price manipulation. (Batt R et al, 2013 )

The subject of Financialisation is relatively new, where neoliberalism and globalisation has extensively been researched and discussed. There have been different meanings over the years of what Financialisation actually means, and Krippner summarises the discussion, some writers use the term ’Financialisation’ to mean the dominance of ‘shareholder value’ as a mode of corporate governance; some use it to refer to growing dominance of capital market financial systems over bank-based financial systems; some follow Holferding’s lead and refer to it as increasing political and economic power of a particular class grouping: the rentier class; for some it represents the expansion of financial trading with a variety of new financial instruments; finally, for Krippner the term refer to a ‘pattern of accumulation in which profit making occurs increasingly through financial channels rather than through trade and commodity production.’ (Krippner 2004:14)

All these definitions capture some aspect of the phenomenon we have called financialisation. A widely commended definition of financialisation is offered by Epstein (2001,p.1): “Financialisation refers to the increasing importance of financial markets, financial motives, financial institutions, and financial elites in the operation of the economy and its governing institutions, both at the national and international level.” Financialisation is transforming the economic system at both macro and microeconomic levels. It’s key impacts are (1) elevate the significance of the financial sector (Growing size of capital, credit and derivatives markets) relative to the real sector; (2) transfer income from the real sector to the financial sector; and (3) contribute to increased income inequality and wage stagnation. (Palley et al, 2013)

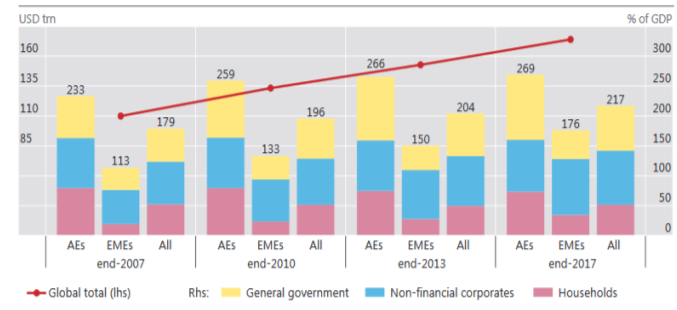

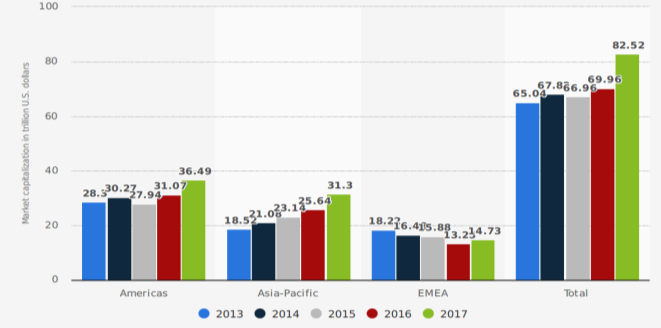

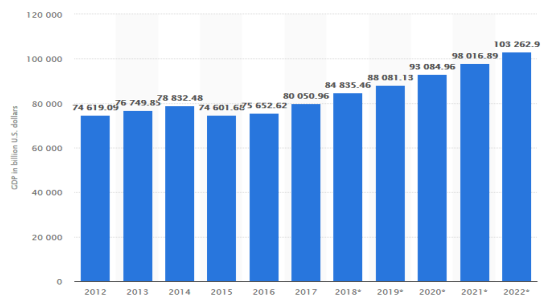

The next question to ponder is why does finance matter? Since the 1970s, finance matters because continuous financial innovation has led to new relations with financial markets that mediate the macro-economy and our experience as individual subjects. (Erturk et al, 2008) For example, in the late 1970’s the financial innovation of new instruments called derivatives from nothing lead to a value to more than $595 million trillion in terms of amounts outstanding by 2018 (BIS,2018). In addition, deregulation, liberalisation and globalisation of financial markets, and technological advance since 1980s has led to the size of finance to grow multiples of global GDP. As most of the economic growth in finance has been debt-driven, asset inflation-driven creating inequality and instability. Figure 3 shows how the global debt 110% of GDP at the end of 2007 and risen to approximately 350% of GDP at the end of 2017. As debt increases this leads to a reduction in money spent on good and services which in hindsight slows down the economy causing a reduction in government taxes, thereby leading to more borrowing. In addition, we can see that the financial economy (figure 2) is continuing to grow more than the real economy (Figure 3), as it increased from 28.3 trillion US dollars to approximately 36.5 trillion U.S dollars in 2017, whereas the real economy (Figure 3) has merely grown approximately by 5 trillion US dollars. As people are in more debt, they search for high yields by investing in stock markets, corporate and sovereign bonds, and derivative markets, leading to the financialised global economy to continue growing greater than the real economy. Therefore, this increases the risk of financial crisis creating uncertainty and instability.

Figure 1.(Source: BIS, 2018) Chart showing the global debt in USD tn to % of GDP

.

Figure 2. (Source: WFE, 2018) Global domestic equity market capitalisation from 2013 to 2017, by region (In trillion US. Dollar)

Figure 3. (Source: IMF, 2018) Global gross domestic product (GDP) at current prices from

2012 to 2022 (In billion U.S dollars.

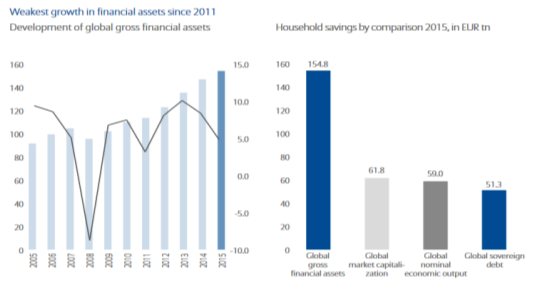

Financialisation is not only a macroeconomic phenomenon that is only observed in financial markets but also affects household balance sheets and wealth. (Ertuk et al, 2008) As stagnation of payments, income inequalities, and less labour security, and insecure employment have changed household behaviour. As a result, there is a shift in household savers to switch from bank deposits and government bonds into potential high yielding riskier assets that could go up or down in value. We can see in

(figure 4)

shows that from 2005 to 2015, household saving almost doubled, and are growing at an average rate of 5.7%. In addition, we can see in

(figure 5)

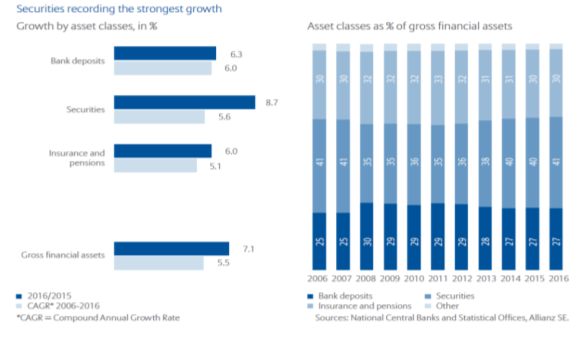

that majority of household financial assets are in securities which are of higher risk compared to band deposits and continued to grow between 2008-2015.

Figure 4 – (Source: Allianz, 2017) One chart showing household savings in financial assets from 2005-2015 and the other showing household savings

by comparison 2015, in EUR tn.

Figure 5-

(Source: Allianz, 2017) one chart showing the growth by asset classes in % during 2016/2015, including another chart showing the breakdown of each asset class from 2006-2016.

Financialisation has evolved within the National Health Service (NHS). First, since the 1980’s the NHS has been subject to continuous reforms to introduce market like structures, which has been accelerated by the introduction of the 2012 Health and Social Care Act (HSCA). The growing financial deficit in the NHS created a platform for the HSCA reform, which has led to greater private sector intervention, and for NHS trusts to increase revenue from private sources. The neoliberal policies in health are opening pathways for more financialised structures in the provision of health in the UK. Four key “mechanisms” of Financialisation prevail in the NHS in England, (1) internal “markets” and financial structure; (2) NHS funding for non-NHS providers; (3) Private income for NHS providers; (4) Private finance initiative (PFI). (Bayliss, 2016)

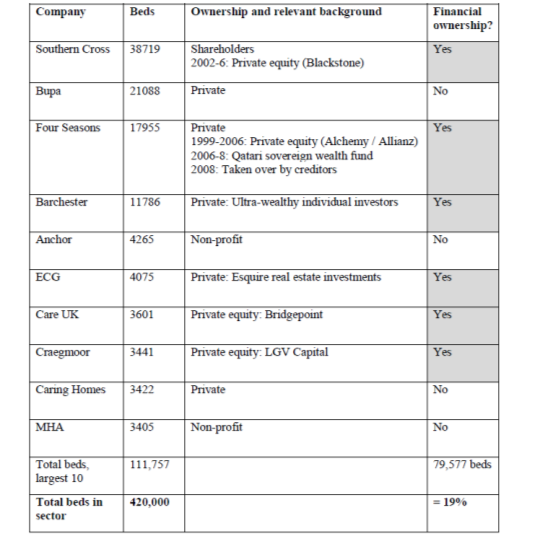

The HSCA has fuelled the growth of health service contracts to private companies, including through the private finance initiative, with private health providers often backed by institutional financial investors. (Bayliss, 2016). Prior to the 2012 HSCA, an internal market already existed in health provision with a division between purchasers and providers of healthcare, with mainly providers of care being public NHS hospital and community trusts. However, following the 2012 HSCA there has been a development of a competitive tender with all providers, including for-profit health companies as well as NHS providers, all treated equally. (Bayliss, 2016) The “purchasers” or commissioners of care consist of 209 clinical commissioning groups (CCGs) whom are responsible for about 60% of the NHS budget (Bayliss,2016) The British Medical journal stated following the HSCA in 2014, 1149 contracts (33% of total) were to private sector providers, 335 (10%) to voluntary and social enterprise, 100 (3%) to joint ventures and local authorities, and 1910 (55%) of contracts were to NHS providers. (BMJ, 2014) Many of these private sector companies are listed on the stock exchange and backed by private equity investors who engage in financial practices to maximise shareholder returns. For example, Financialisation had disastrous results in once case. The Southern cross Healthcare group was bought by Blackstone (private equity firm), in 2004, which then implemented a “sale and leaseback” operation. (Horton, 2017) The care home properties were sold to a sperate company owned by Blackstone called NHP, and then leased back by Southern Cross, and was later sold for £1.1 Billion to a fund backed by Qatar Investment authority. (Bayliss, 2016) Post financial crisis NHP could not afford payments to NHP, including being reported as providing poor care standards by the CQC, which lead to permanent closure in October 2011. In an enquiry, the company’s financial structure was linked to poor care and the deaths of five residents. (Bayliss, 2016) In addition, other private equity investors are present from the likes of Advent international investing in mental health service in the NHS, Cinven investing in the Spire the second largest private hospital operator in England, including health companies from overseas where private provision is more entrenched, such as the Hospital Corporation of America (HCA) the largest for profit hospital chain in America. (Appendix 1) As more private companies enter the healthcare sector, this will transform the provision of health being a local community service to several global investment portfolios of international private finance. (Bayliss, 2016) Ideally, we need to stop this financialisation within the NHS as it can have detrimental affects to patient care, such as in the case of Southern Cross, and so more services to be provided by local NHS trusts than private companies that engage in financial practice to maximise shareholder returns.

Overall, too much finance damages economic stability and growth, changes the distribution of income, undermines confidence in the market economy, and manipulates politics. So, what is to be done? As Prof Zingales argues, if those financiers believe they can do whatever they want trust will break down, and we need to be able to trust financiers. (Wolf, 2015) Secondly, reduce incentives for excessive finance, such as tax deductibility of interest, and thirdly get rid of the too big to fail and too big to jail. (Wolf, 2015) However, the likelihood of this happening is unlikely as the markets are exposed to continuous corruption, and the large multinational companies are deeply involved in government to ensure shareholder-oriented capitalism. for example, funding political campaigns ensuring they are unaffected by new regulations. If nothing is done and we allow the financialised global economy to grow exponentially, then we should expect uncertainty and instability with an increase number of financial crises.

Topic 6 Critical drivers of the modern business environment.

Digital globalisation, including the use of ‘big data’ and algorithms have become critical drivers of the modern business environment. Soaring flows of data and information now generates more economic value than the global good trade (Manyika et al, 2016). The world is now more connected than ever. The rapid increase in the cross-border bandwidth has grown 45 times larger since 2005 and is projected to increase 9 times over the next 5 years (Manyika et al, 2016) For example, in 2005 the cross-border interregional bandwidth was 1.6 gigabits per second, increasing to 70.5 gigabits per second in 2014. (Manyika et al, 2016) Digital globalisation has opened the doors for developing counties, start-ups and SMEs, enabling them to compete against the advance companies and large multinational companies. Using digital platforms and tools companies are connected in real time and are becoming leaner, more efficient and can compete in fast growing markets. McKinsey report that over a decade, all types of digital flows acting together have raised world GDP by 10.1% amounting to $7.8 trillion in 2014 alone, and data flows account for $2.3 trillion of this impact. (Manyika et al, 2016).

The power of big data includes the epistemological and ontological possibilities of being able to simultaneously derive breadth and depth, quantitative and qualitative, insights from the same data-set, enabling us to generate insights thatwere previously impossible, with the aura of truth, objectivity and accuracy. (McFall et al, 2017) Companies now have the capacity to search, aggregate, and cross-reference large data sets allowing them to understand their customer and sell products which are tailored to their needs. For example, Wonga one of the largest UK payday lending companies use digital data techniques that include algorithms combining 1000s of datapoints, enabling them to listen to their customer and target their product offers accordingly. (McFall et al, 2017) The use of big data has a variety of functions for modern day business, including improving their efficiency. For example, financial companies reach a decision in lending within minutes through using set data points and algorithms.

Customer needs are constantly changing and for companies to be competitive and continue growing they need to understand who their customers are, including their journey, changing needs, and requirements. The quality of the relationship is essential to a marketing strategy, which uses the combination of qualitative and quantitative data points and algorithms to work out who their customers are, and especially predict what they might do next. For example,Amazon in 2015 patenting ‘anticipatory shipping’, a logistics system designed to ship products before they are purchased, so when the customer makes the purchase it can be instantly shipped and delivered within the promised time frame. (McFall et al, 2017) In addition, Customer relationship management systems ‘mass personalise’ consumers into individual profiles and deploy feedback technologies that automate consumption and modify marketing systems. (McFall et al, 2017)

Now let’s look at how digital technology can help transform the NHS. Digital technology has the potential to revolutionise the way patients access services, improving efficiency and co-ordination of care, and support people to manage their health and wellbeing. (Honeyman et al, 2016) McKinsey estimated that modern health systems can save between 7-11.5 % of their health expenditure. (London et al, 2016) In addition, a study commissioned by NHS England estimated annual savings of £10 billion or more after investing more in a digitised NHS. (Dunhill, 2015) Achieving this can be done in several ways as suggested in the Kings fund study ((Honeyman et al, 2016), include the following:

- Data captured by digital technologies could improve service planning, help align capacity more closely with demand.

- Advance medial practice- for example, using advanced analytic techniques, such as machine learning to support clinical decisions and personalise treatment based on analyses of people’s genomes.

- Put patients in control to take a more active role in their own health and care, by providing access to apps and resources with high-quality information including peer support online.

- For clinicians, it can help reduce the time spent accessing patient information; remote monitoring enables clinicians to better understand the patient progress and helps deliver better health outcomes.

- IT, data systems and information sharing are critical in delivering integrated care and can improve the co-ordination of care delivered by professional across different organisations.

A more digital advanced NHS will improve the quality, efficiency and access to healthcare services. A digitised secondary care system is underway, as the appointment of a national chief clinical information office (CCIO) to oversee NHS clinical digitisation efforts, including every trust to have a CCIO to lead development of a more digitised NHS trust. To ensure this happens the Department of Health and NHS England have provided additional funding and a phased approach to implementation with a target for all trusts to reach digital maturity by 2023. (Honeyman et al, 2016) It is imperative the NHS achieves these targets to ensure that it is digitally advance and continues to be able to provide one of the best health care services in the world.

The use of artificial intelligence is a critical driver in modern day health care, as it will help improve quality, management, efficiency of patient health outcomes. For example, Deepmind a leading artificial intelligence company has developed AI technology that analyse optical cohenrence tomography scans (OCT), which automatically detects eye conditions in seconds, and prioritises those patients in urgent need of care. (Deepmind, 2016) This AI technology is currently being audited at Moorfeilds Eye Hospital NHS trust in partnership with clinicians. It has been found to help improve patient care by reducing waiting times, and prioritise those patients that require treatment first. (Deepmind, 2016)

The drive for healthcare to become digitised is evident throughout the world, as the size of the global market for digital health is continuously growing and is currently expected to be worth £43 billion, including £2.9 billion in the UK which makes up 7% of the global market. (Deloitte, 2015) Digital health systems represent the largest market both globally and, in the UK, where they contribute to 66% of digital health sales. (Deloitte, 2015). Digital globalisation of healthcare will continue to grow, but the fact of it being easy to capture, share and use data for direct care and secondary use poses a risk. If there is any lack of understanding on part of patient or staff to how it is handled can be obstacle to sharing data and hinder the progress in digital health-technology.(Honeyman et al , 2016) The vast amounts of data collected by the NHS, if shared using strong safeguards, has huge potential to support improvements in care and research. The benefits include improving an individual’s clinical care and protecting, and linking data from different sector to enhance our understanding of the populations health more broadly. (Honeyman et al, 2016) To tackle the issue of consent and security, and increase public confidence, Dame Fiona Caldicott, National data Guardian for Health and Care, proposed 10 new data security standards to apply to every organisation handing health and social care information, including a new consent and opt-out model for sharing of confidential patient data. (Honeyman et al, 2016)

Overall, the government consider better use of information and digital technology to be a critical driver of the NHS moving forward in the world of healthcare,and have set out an ambitious vision that seeks to digitally transform healthcare services within the UK. However, the backdrop of this occurring would be the unprecedented financial and operational pressures within the NHS organisations, and so in order to achieve cost savings from digitisation in health care in the UK, will require investment and will take time to deliver.

References

- Figure 4 and 5: Allianz (2017). [online] Allianz.com. Available at: https://www.allianz.com/content/dam/onemarketing/azcom/Allianz_com/migration/media/economic_research/publications/specials/en/AGWR2016e.pdf [Accessed 30 Dec. 2018].

- Batt, R. and Appelbaum, E., 2013. The impact of financialization on management and employment outcomes.

- Bayliss, K., 2016. The Financialisation of Health in England: Lessons from the Water Sector.

- Bis.org. (2018). [online] Available at: https://www.bis.org/publ/arpdf/ar2018e.pdf [Accessed 30 Dec. 2018].

- Figure 1: Bis.org. (2018). [online] Available at: https://www.bis.org/publ/otc_hy1810.pdf [Accessed 30 Dec. 2018].

-

BMJ (2014) “A third of NHS contracts awarded since health act have gone to private sector, BMJ investigation shows”

http://www.bmj.com/content/349/bmj.g7606

-

Deloitte, M., 2015. Digital health in the UK: an industry study for the office of life sciences.

Deloitte Creative Studio

. - Dunhill L (2015). ‘NHS England: digital plans “could save £10bn”’. Health Service Journal, 17 June.

-

Epstein, G.A. ed., 2005.

Financialization and the world economy

. Edward Elgar Publishing. - Epstein, G., “Financialization, Rentier Interests, and Central Bank Policy,” manuscript, Department of Economics, University of Massachusetts, Amherst, MA, December 2001.

-

Erturk, I., Froud, J., Johal, S., Leaver, A. and Williams, K., 2008. General introduction: Financialization, coupon pool and conjuncture.

Financialisation at work

, pp.1-44. -

Honeyman, M., Dunn, P. and McKenna, H., 2016. A Digital NHS.

An introduction to the Digital agenda and plans for implementation

. -

Horton, A.E., 2017.

Financialisation of Care: Investment and organising in the UK and US

(Doctoral dissertation, Queen Mary University of London). -

Figure 3:

IMF. n.d. Global gross domestic product (GDP) at current prices from 2012 to 2022 (in billion U.S. dollars). Statista. Accessed December 28, 2018. Available from

https://www-statista-com.manchester.idm.oclc.org/statistics/268750/global-gross-domestic-product-gdp/

. -

Krippner, G., 2004. What is financialization?.

University of California, Los Angeles

. -

London T, Dash P (2016). Health systems: Improving and sustaining quality through digital transformation [online]. McKinsey & Company website. Available at:

www.mckinsey.com/businessfunctions/digital-mckinsey/our-insights/health-systems-improving-and-sustaining-quality-through

– digital-transformation?cid=digistrat-eml-alt-mip-mck-oth-1608 (accessed on 28 December 2019). - Manyika, J, et al. (2016). Digital globalization: The new era of global flows. [online] McKinsey & Company. Available at: https://www.mckinsey.com/business-functions/digital-mckinsey/our-insights/digital-globalization-the-new-era-of-global-flows [Accessed 30 Dec. 2018].

- McFall, L. and Deville, J., 2017. The market will have you: the arts of market attachment in a digital economy.

-

Palley, T.I., 2013. Financialization: What it is and Why it Matters. In

Financialization

(pp. 17-40). Palgrave Macmillan, London.

-

Figure 2:

WFE. n.d. Global domestic equity market capitalization from 2013 to 2017, by region (in trillion U.S. dollars). Statista. Accessed December 28, 2018. Available from

https://www-statista-com.manchester.idm.oclc.org/statistics/376681/global-equity-market-capitalization-by-region/

. - Wolf, M. (2015). Why finance is too much of a good thing | Financial Times. [online] Ft.com. Available at: https://www.ft.com/content/64c2f03a-03a0-11e5-a70f-00144feabdc0 [Accessed 30 Dec. 2018].

Appendix 1

Table 1: (Source: Horton, 2017) Ownership of the ten largest providers of care homes, Jan 2011.

PLACE THIS ORDER OR A SIMILAR ORDER WITH NURSING TERM PAPERS TODAY AND GET AN AMAZING DISCOUNT